Single tenant net leased deals, an area that never truly ceased activity, has been leading the comeback among property classes. RetailTraffic's recent story is in-line with what we've been seeing in the market as well, with cap rate compression being lead by net leased opportunities. Though many owners who bought in 3 or more years ago at sub-7% cap rates are hesitant to lose on the sales side today, new development and even some of those hold-outs are recognizing interest is back and sub-8% is doable. As the article points out, cap rates for a Walgreens are probably around 7.75%, though we see that compressing over the next 6-9 months by up to 50 basis points.

Cincinnati Redevelopment to Add Residence Inn

Another sign the real estate market is coming back, not least the economy, is new hotel development, this time in downtown Cincinnati. The Business Courier is saying construction has already begun on coverting an old office tower into 134-unit Residence Inn.

High Definition Video Home Tours

Remember the days of waiting several minutes for a jerky virtual tour to load? You'll see them every now and then online. The stitched together jpeg files that let you see a room by changing the direction by clockwise or counterclockwise. Those days are already over, the future now belongs to high definition video home tours.

Why settle watching some outdated low resolution tour when there are plenty of professional grade high definition video tours out there. As a home owner, why would you list your home with someone that is using old technology to market your home?

If you are looking for high definition alternative, I recommend High Five Productions for all of your Las Vegas Video services.

Why settle watching some outdated low resolution tour when there are plenty of professional grade high definition video tours out there. As a home owner, why would you list your home with someone that is using old technology to market your home?

If you are looking for high definition alternative, I recommend High Five Productions for all of your Las Vegas Video services.

Proof - CMBS is Back

Globest.com reported the closing of a $31.3 million CMBS loan through JP Morgan Chase to a Michigan REIT. Though exciting that CMBS is quickly coming back , keep in mind it will take some time to achieve the terms that were common 2+ years ago. This loan closed on just 60% LTV and a 10 year term. But for non-recourse debt right now, the LTV isn't getting too much better, with life companies at gnerally 65%. As our Debt & Equity team from Detroit has pointed out, it also takes very strong sponsorship, such as a large REIT, to get CMBS done right now.

Healthcare Bill Could Equal 60,000,000 new MOB SF

The historic healthcare bill signed into law this week is going to have a significant impact on commercial real estate, whether specifically intended or not. There is going to be a lot of discussion on what that impact will be as the months and years roll by. Co-Star has an article on the bill's impact, and at one point quotes an industry player that the bill could ultimately lead to 60,000,000 more feet of MOB based on the number of new patients entering the rolls of the insured. On the flip side, the bill contains strong prohibitions on physician-owned hospitals, which will have a significant impact on current and future developments and currently existing hospitals.

First Time Home Buyer Tax Credit Extension Ending

The First Time Home Buyer Tax Credit extension is coming to an end next month for most people. The extension gives certain Federal employees and military personnel additional time to take advantage of it. For the rest of us, to qualify you must be in escrow on a property (and meet the other requirements of course) before May 1st.

There has been a lot of debate over whether the tax credit has helped sales. I think you'll find a lot of support among those buyers that have been able to take advantage of the credit and have actually received their refund. Feel free to leave your thoughts in a comment.

If you would like listings of Las Vegas homes for sale, call 702-493-8033.

Garden Therapy

Some have a green thumb and forget all the problems taking care of plants and flowers in a garden or a terrace. But even those who have never tried it, can try this therapy, achieving great advantages.

The Garden Therapy, or ortoterapia, is a genuine alternative medicine for 'soul and body.

Founded in 1300 when Irish monks tended gardens to combat depression, but is now used throughout the world, especially in rehabilitating people with Alzheimer's, disabled and as supportive therapy in the treatment of addictions.

This form of natural medicine has proved very useful in treating forms of stress and anxiety, more and more present today.

Busy with a piece of land or of any vessel combines an excellent exercise to practice relaxation.

In addition, the garden ol 'garden requires constant care that requires commitment and passion.

Verder satisfaction from growing the plants and nurtures a deep trust even the most pessimistic.

Herbs

If you are new to gardening, but want to use this method as stress, one can begin to cultivate herbs: they are the most robust and easy to grow even on the balcony.

Their scent communicate messages that awaken awareness and invite you to establish a relationship with them.

In one corner of the balcony, try putting those most important to health: melissa sleeping good for digestion, marjoram, thyme against bronchitis, rosemary to have more energy.

The Garden Therapy, or ortoterapia, is a genuine alternative medicine for 'soul and body.

Founded in 1300 when Irish monks tended gardens to combat depression, but is now used throughout the world, especially in rehabilitating people with Alzheimer's, disabled and as supportive therapy in the treatment of addictions.

This form of natural medicine has proved very useful in treating forms of stress and anxiety, more and more present today.

Busy with a piece of land or of any vessel combines an excellent exercise to practice relaxation.

In addition, the garden ol 'garden requires constant care that requires commitment and passion.

Verder satisfaction from growing the plants and nurtures a deep trust even the most pessimistic.

Herbs

If you are new to gardening, but want to use this method as stress, one can begin to cultivate herbs: they are the most robust and easy to grow even on the balcony.

Their scent communicate messages that awaken awareness and invite you to establish a relationship with them.

In one corner of the balcony, try putting those most important to health: melissa sleeping good for digestion, marjoram, thyme against bronchitis, rosemary to have more energy.

{kind=link}

Relocating Company Breaking Ground in Brecksville

Some good news for Northeast Ohio was published by the Toledo Blade today - True North Energy will be building their new corporate headquarters in Brecksville. The site is set to be completed in May 2011. Many in Northeast Ohio will recognize the True North brand at Shell stations. True North is 50% owned by Shell. It's good to see companies moving into the region, though it's a little surprising True North is doing a build-to-suit. Office space right now is priced well below replacement cost. Roughly speaking, new office construction can be about $150 SF, while equivalent Class A office might be $100 SF. But like Eaton, True North must put some real value on having its own designed campus.

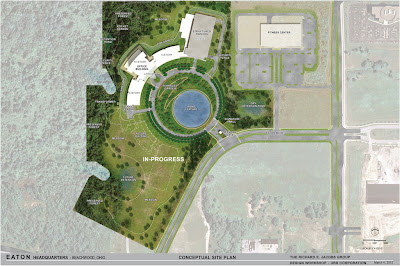

Eaton's Sprawling Beachwood Campus - A Giant Pond?

Eaton Corp. and Richard E. Jacobs Group, the lead developer of the project, submitted some site renderings of the proposed project at a Council meeting this past Monday night, per Plain Dealer reporting. As most know, Eaton has bailed on downtown and is developing a new 53-acre campus in Chagrin Highlands. They are seeking a variance to eliminate nearly 1,300 parking spots required under current zoning. The two site renderings submitted by Eaton are posted here. With some 2 miles of trails, it looks like a pretty nice campus (though one commentator suggested the giant pond made the campus look like a big toilet, which I'm sure is not the concept the design team had in mind). It's just too bad our Central Business District pushes companies like Eaton away. The crazy thing is that Cleveland will still get 50% of the tax revenue. This is what a PD reporter had to say in the comment section of the article:

But in reality, how much is Cleveland really losing from employee income tax, meals tax, hotels and entertainment, etc., etc. Not too mention the fact yet another major corporate business is leaving the CBD. At least it's still in Northeast Ohio.

But in reality, how much is Cleveland really losing from employee income tax, meals tax, hotels and entertainment, etc., etc. Not too mention the fact yet another major corporate business is leaving the CBD. At least it's still in Northeast Ohio.

(Photos courtesy of The Plain Dealer/cleveland.com, as obtained from Eaton/Richard E. Jacob Group)

From reporter Michelle Jarboe:

.... under a preexisting joint economic development agreement, Cleveland will receive a 50 percent cut of the income tax revenues generated by Eaton from the Chagrin Highlands campus, even though the property is in Beachwood.

(Photos courtesy of The Plain Dealer/cleveland.com, as obtained from Eaton/Richard E. Jacob Group)

Senior Housing Update - Rents Up, Occupancy Slightly Down

NIC recently released its latest data on the senior care market. NAREIT also published a story on the results. The data showed slowing activity in construction, slight declines in occupancy, but a small uptick in rents. These results seem to be in line with the regional activity we're seeing. The attached chart highlights changes from the 4th quarter in 2008 to 2009

NIC recently released its latest data on the senior care market. NAREIT also published a story on the results. The data showed slowing activity in construction, slight declines in occupancy, but a small uptick in rents. These results seem to be in line with the regional activity we're seeing. The attached chart highlights changes from the 4th quarter in 2008 to 2009 Changes in Mark-to-Market? FASB proposes new standards.

The Financial Accounting Standards Board is proposing that banks expand their use of mark-to-market accounting to include loans and other financial assets, as reported by the WSJ. Though marking assets to market values can make sense in a vaccum of financial analysis, the real world implications are huge. The problem is that markets, like historical costs, do not always represent the real value. Bigger than that though is the fact that financial statements can only provide limited, historical information. In a market moving and changing as fast as today's, trying to rely on information that can be up to several months old and that provides no predictive insight on where values will be, can create major issues, as we've seen. For example, making banks adjust their minimum capital based on asset values that may be outdated by the time their published doesn't seem like a good use of information.

Debt - Back in Action in the Midwest

The below is the latest update from CBRE's Debt & Equity team that covers Michigan, Ohio, and Indiana. The important points seem to be 1) financing is available, and 2) though slightly higher rates than borrowers might like, its non-recourse.

Permanent Financing for Stabilized Assets

We continue to see signs of life in the credit markets. Banks largely remain on the sidelines, with the exception of community banks and credit unions. Life companies continue to cherry pick financing trophy assets in trophy markets with trophy sponsors. However, portfolio and balance sheet lenders are offering an alternative way to finance stabilized properties on a non-recourse basis.

I wanted to spotlight a loan program that will finance deals in the Midwest:

• $5 - $50 million

• 3-5 year term, may go longer in select cases

• Up to 75% LTV on “as is” value

• Acquisition or refinancing

• Stabilized multi-family, retail, office and industrial properties

• 7.0% - 8.5%

• Amortization up to 30 years

• Non-recourse

• 1.00% origination fee to lender

• Escrows for taxes, insurance, replacement reserves, tenant improvements/leasing commissions and immediate repairs

Permanent Financing for Stabilized Assets

We continue to see signs of life in the credit markets. Banks largely remain on the sidelines, with the exception of community banks and credit unions. Life companies continue to cherry pick financing trophy assets in trophy markets with trophy sponsors. However, portfolio and balance sheet lenders are offering an alternative way to finance stabilized properties on a non-recourse basis.

I wanted to spotlight a loan program that will finance deals in the Midwest:

• $5 - $50 million

• 3-5 year term, may go longer in select cases

• Up to 75% LTV on “as is” value

• Acquisition or refinancing

• Stabilized multi-family, retail, office and industrial properties

• 7.0% - 8.5%

• Amortization up to 30 years

• Non-recourse

• 1.00% origination fee to lender

• Escrows for taxes, insurance, replacement reserves, tenant improvements/leasing commissions and immediate repairs

One Year Ago

Lehman Brothers went out of business and the world seemed to stop turning for a few moments. There was common opinion that the financial markets and anything related would continue a free fall that had started only months earlier. The Dow Jones Average had a nearly 45 degree angle of descent going. It was not pretty and it was darned hard to find anyone who thought it was.

There were a few bold souls though who started buying again, figuring that good companies were not just good in good times but also in not-so-good times. Companies like Proctor & Gamble, Walmart, and Chevron, to name a few. These are not sexy new start-up companies or high-tech about to unveil the new new thing but stalwart companies that were trading at a pretty good price, especially compared to the not-too-distant highs from not that many months earlier. What had changed? Had the companies become over-levered or outmoded? No, they simply were caught on the same discount ride down that the entire market was on. If you bought last March you are pretty happy today. Your reward for defying common wisdom is a return of somewhere around 50%. Not too shabby.

So where are we with Apartment investing? We have had at least a year of negative news, rent declines, vacancy increases, locally watched the demise of WaMu, and several real estate kingpins got into debt trouble. The surrender of Stuyvesant in New York to the lenders is likely the largest apartment investment default in history, over $5 Billion. Does this mean apartments are done? About as much as Proctor & Gamble is.

It has been a very long time since an investor could buy an apartment building in any decent area in Seattle and get positive leverage. With debt rates around 6 and CAP rates near the same level it is one of the best times in the past 20 years to buy apartment buildings again. The same view that an investor would have for Johnson & Johnson, except that in apartment investing you get to use debt, is the approach I think is wise for apartment investing today: buy high quality locations and buildings and they will perform well over time. They will not go up like a rocket but neither will they fall like an over-leveraged investment house like Lehman Brothers or WaMu.

If you could have March 2009 all over again what would you buy? I think we are at that same moment for Apartment investing today. We won’t know for sure for many months and the common wisdom is that it is better to wait to see what happens. By then common wisdom will have worked against you again.

Challenges in Cleveland's Real Estate Market

The Plain Dealer, Cleveland largest newspaper, published a mildly interesting article today. Anyone that has read this blog should know, probably more intimately than most, the general problems and issues with, and potenital fixes needed for, commercial real estate. And not just in Cleveland. But its good to know what the non-real estate news sources are writing about CRE anyway.

Ohio - Leading the Economic Development Charge - Again!

Site Selection Magazine has awarded Ohio its Govenor's Cup for the fourth year in a row. As the cover story indicates, "Site Selection’s annual Governor’s Cup award recognizes the state with the most new or expanded private-sector capital projects as tracked by publisher Conway Data Inc.’s New Plant Database." We have included the story's "Selected Ohio Projects" chart to the right and a state-by-state look at three years of development activity below.

Site Selection Magazine has awarded Ohio its Govenor's Cup for the fourth year in a row. As the cover story indicates, "Site Selection’s annual Governor’s Cup award recognizes the state with the most new or expanded private-sector capital projects as tracked by publisher Conway Data Inc.’s New Plant Database." We have included the story's "Selected Ohio Projects" chart to the right and a state-by-state look at three years of development activity below. Site Selection Score Card

Thought This Article Was Interesting, You Might Too

Does Another Wave of Foreclosures Loom?

Not likely, but you won't hear that from the media

Just as the media hyped the real estate bubble, reporters and pundits are now riding an alarmist wave of foreclosure news. Case in point: A recent newspaper headline warned, “Another Wave of Foreclosures Looms — Ballooning Payments Put Mortgages at Risk, Posing New Setback to Market.”

The concern at the heart of the article: An estimated 70% of Option ARMs will reset by 2011. Option ARMs are adjustable-rate mortgages that give the borrower choices regarding how much to pay each month.

At first glance, that statistic sounds scary — it represents $189 billion worth of loans. But is it really all that bad? Let’s find out.

There are 75.6 million owner-occupied homes in the U.S., according to the Census Bureau. Of those homeowners, 61% have a mortgage.

The article states that Option ARMs make up 1.3% of all mortgages. In other words, we’re talking about a little more than 600,000 mortgages. If 70% of those loans reset, the figure is about 422,000 mortgages. And don’t assume that those homeowners are going to default merely because their loans reset. “Reset” means the interest rate will adjust to new rates — and rates are now lower than they were three years ago when these loans were obtained, not higher. That means many of these homeowners might enjoy lower payments, not higher ones. Say half of the resetting loans prove unaffordable. Even that doesn’t mean the homeowners will necessarily default. Many, after all, will be able to figure out a way to keep making their payments.

But suppose half of them actually do go into default. In that case, we’re talking about 211,000 loans defaulting — spread over the next two years. That’s about 100,000 loans defaulting next year — out of 75.6 million homeowners.

That’s 0.14% of all homes. And that is supposed to support a headline that reads, “Another Wave of Foreclosures Looms — Ballooning Payments Put Mortgages at Risk, Posing New Setback to Market.” Either the writer of that article is deliberately attempting to scare readers needlessly, or the writer fails to understand the true nature of the situation. Incompetent or irresponsible? Either way, you shouldn’t draw incorrect conclusions from this story — and stories like this one are all too common.

-Article Written by Ric Edelman

Light Reading

I just read an article from one of my competitors in which the guy suggests how wise it is to sell well located Seattle apartment buildings and move the equity into a higher yielding apartment building in the Tri Cities. I was stunned. I had just recently been thinking that if the current market has reminded me of anything it is at least the simple understanding that quality locations always fair better in soft markets.

Maybe that makes me a contrarian, at least to what my competitor is promoting. This also reminds me of the far too popular TIC deals that a few people went into, usually to their great disappointment.

As far as I can tell, and my experience is limited to only about 25 years of being an apartment broker in Seattle, the best areas always cost more but are always worth it. I suppose tempting people with the idea of higher cash flow is one way of stirring up some business but I kind of figure that is the last time that agent will do business with that customer. Solid investments are usually boring but therein lies the beauty, at least as far as I am concerned.

Maybe that makes me a contrarian, at least to what my competitor is promoting. This also reminds me of the far too popular TIC deals that a few people went into, usually to their great disappointment.

As far as I can tell, and my experience is limited to only about 25 years of being an apartment broker in Seattle, the best areas always cost more but are always worth it. I suppose tempting people with the idea of higher cash flow is one way of stirring up some business but I kind of figure that is the last time that agent will do business with that customer. Solid investments are usually boring but therein lies the beauty, at least as far as I am concerned.

Subscribe to:

Posts (Atom)